- Email:sales@siny.hk; angela@siny.hk

Source:LightCounting

LightCounting releases an updated Optical Components forecast

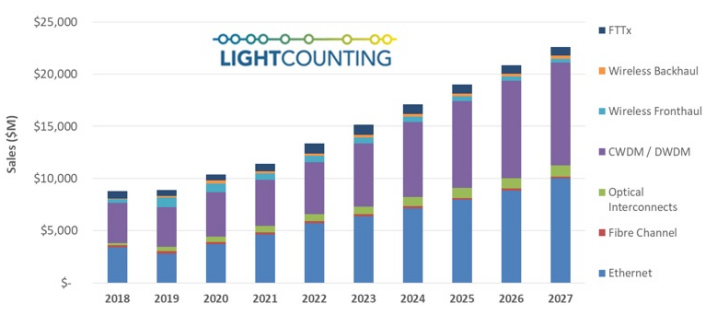

The optical communications industry entered 2020 with a very strong momentum. Demand for DWDM, Ethernet, and wireless fronthaul connectivity surged at the end of 2019, and major shifts to work-at-home and school-at-home in 2020 and 2021 due to the COVID-19 pandemic created even stronger demand for faster, more ubiquitous, higher reliability networks. While supply chain disruptions continued, the industry was able to largely overcome them, and the market for optical components and modules saw strong growth in 2020 and 2021, as shown in the figure below.

We believe the transceiver market is on track for another year of strong (17%) revenue growth in 2022, after increasing by 9% in 2021, and 17% in 2020. Demand for optics is strong across all market segments, and continuing bottlenecks in the global supply chain probably created some extra demand (over-ordering) and certainly moderated price declines, contributing to higher-than-expected growth in 2021 sales and an increased forecast for 2022-2027, illustrated in the figure below.

The latest forecast projects a 12% CAGR in 2022-2027, not very different from the 13% CAGR in the forecast published in October 2021. Strong sales of DWDM and Ethernet optics accounted for most of the gains last year and these segments are projected to lead the growth in 2022-2027. Sales of optical interconnects, mostly Active Optical Cables (AOCs), will also increase at double digit (10%) CAGR over the next 5 years. Wireless fronthaul is one area of weakness, with price declines coupled with cyclical declines in unit shipments resulting in negative sales growth.

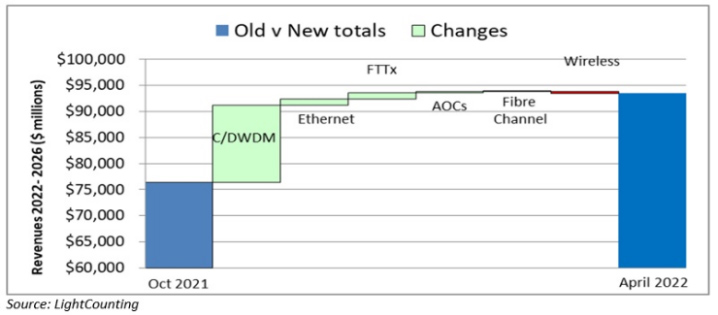

Forecast changes due to Methodology and other factors

The waterfall chart below shows changes in the forecast for aggregated 5-year sales, compared to the one published in October 2021. Two methodology improvements made in 2022 account for some of the changes. These are:

In the DWDM segment, we no longer forecast ports separately from pluggable transceivers. The ‘onboard’ 100, 200, 400, 600 & above product categories now include all non-pluggable ports, whether 5×7 subassemblies or line card-based solutions. Compared to the October 2021 forecast, DWDM revenues are now much higher, as they include a much greater number of ports. Due to this methodology change, the baseline unit shipments going back to 2016 are increased as well.

In the FTTx segment, we collected more comprehensive data on network level shipments (OLTs and ONUs), resulting in a significant increase in the 2021 volumes of 10G-PON OLT and ONU optics compared to our October 2021 forecast. This increase in the baseline carries through to the forecast years as well.

The Ethernet forecast was updated in March 2022 in conjunction with the publication of our High-Speed Ethernet Optics report, and is unchanged since then. It is above the October 2021 forecast due to increased volumes for 400G, 800G, and 1.6T products.